On September 18, 2025, the industry did a double-take. Intel and Nvidia announced a deal in which Nvidia would purchase $5 billion in Intel shares while committing to jointly develop multiple generations of custom data centre and PC products. For Intel, it was both a cash infusion and a partnership with thevery company that had outpaced it in AI and accelerated computing — which is abit like a former heavyweight champion accepting corner support from the fighter who knocked him out.

A month earlier, on August 18, SoftBank committed $2 billion to Intel common stock at $23 per share. Behind the scenes, the U.S. government holds a passive, non-voting 9.9% equity stake in Intel, acquired through CHIPS Act grants and the Secure Enclave program.

To a casual observer, these look like endorsements, somehow proof that Intel still has aseat at the table. Look closer, and the picture is gloomy. A company doesn't take a rival’s money, a Japanese conglomerate’s cash, and a government equity stake simultaneously unless it's on life support. If Washington announced itwas scooping up 10% of Anthropic or Google, there would bean uproar. The fact that this happened to Intel with barely a mention in the mass media shows just how far the crown jewel of Silicon Valley has fallen. Intel is now surviving on alliances and subsidies rather than its own momentum.

A Short History of Giants Who Stopped Watching the Clock

Intel’s situation is unique in the details, but the pattern is really quite old. The history of tech is littered with dominant companies that hesitated and got left behind.

Olivetti was Europe’s technology trailblazer — typewriters, calculators, early computers, a design sensibility that made its products objects of genuine desire. Then its lead engineer, Mario Tchou, died suddenly. Leadership changed, priorities shifted, and the computer division was sold to General Electric. Olivetti didn’t disappear overnight; it faded, which is in some ways worse. A company that was once synonymous with innovation became a brand that older Italians remember fondly. The young ones don’t know it at all.

Commodore is an even sadder case, particularly if you were a child in the 1980s. TheAmiga was, by any technical measure, extraordinary for its time — 4096 coloursusing HAM (Hold-And-Modify) mode, 8-bit stereo sound that with expansion cardscould reach CD-quality 16-bit audio at 44.1 kHz, all at a point whenIBM-compatible PCs could manage, at best, a tinny beep. The Amiga wasn’t justcompetitive; it was years ahead, used by designers, architects and musicproducers. And yet Commodore still lost. The IBM-compatible ecosystemaccumulated critical mass — more software, more developers, more corporateadoption — and Commodore’s superior technology became irrelevant because thenetwork had moved elsewhere. Being right about the hardware was not enough.

Atari, forits part, had its own epic fall. The video game crash of 1983 exposed itsvulnerabilities: a flood of poor quality games, overextension into hardware andsoftware with little quality control, and inability to respond when cheaper,better alternatives emerged. From dominating arcades and consoles, Ataridescended into fragmentation, bankruptcy, and finally becoming more a brand ofnostalgia than one of innovation.

Nokia’s fall is the one everyone cites because it is so clean and so brutal. Over 40% of the global mobile phone market, then the iPhone arrived in 2007, and Nokia spent the next several years insisting that its Symbian operating system and its hardware expertise would see it through. They didn’t. What Nokia missed, what it genuinely could not seem to perceive, even as the evidence accumulated, was that mobile had stopped being about phones and started being about ecosystems. Apps, developers, UX, the entire experience of holding a device. Ericsson read the same signals and pivoted away from consumer handsets into infrastructure, which was at least a survivable decision. Nokia’s version of that pivot came too late and too expensively.

Facebook’s near-miss is less discussed because it didn’t actually happen, but it nearlydid. Without the acquisitions of Instagram and WhatsApp, Facebook in the mid-2010s was a platform that younger users were already drifting away from. MySpace had shown what that drift looks like when it completes: fast, irreversible, and followed by a very long silence. Zuckerberg saw it coming and moved. Most of his peers didn’t. And the Metaverse has a daily average human usage of a small town (globally, that is). It was so bad that even Meta’s own staff refused to use it. But, as Youtuber Patrick Boyle,a former hedge fund manager and university professor who delivers masterclasses on financial history and corporate folly with a legendary, bone-dry wit says in his video about the Metaverse (link at the end), the Meta-engineers mastere done particular challenge: maybe they couldn’t equip humans with legs from the get-go, but they managed to outfit Zuckerberg with more charisma than in real life.

The Cost of Institutional Blindness

What these stories share is not just complacency, though that’s part of it. It’s a specific kind of institutional blindness that sets in when a company has been dominant long enough that its past strategy starts to feel like destiny. Olivetti didn’t foresee how PCs would reshape computing. Commodore and Atari thought brand and heritage — and in Commodore’s case, genuine technical superiority — would be enough. Nokia and Ericsson underestimated how quickly platform and ecosystem would replace hardware specs as the battleground. Intel, as we will see, made versions of several of these mistakes simultaneously.

Intel’s Missed Chances

There is a version of the Intel story in which none of this had to happen. The company had the resources, the talent, the manufacturing base, and the brand recognition to have positioned itself for almost any major shift in computing over the past two decades. It missed most of them anyway.

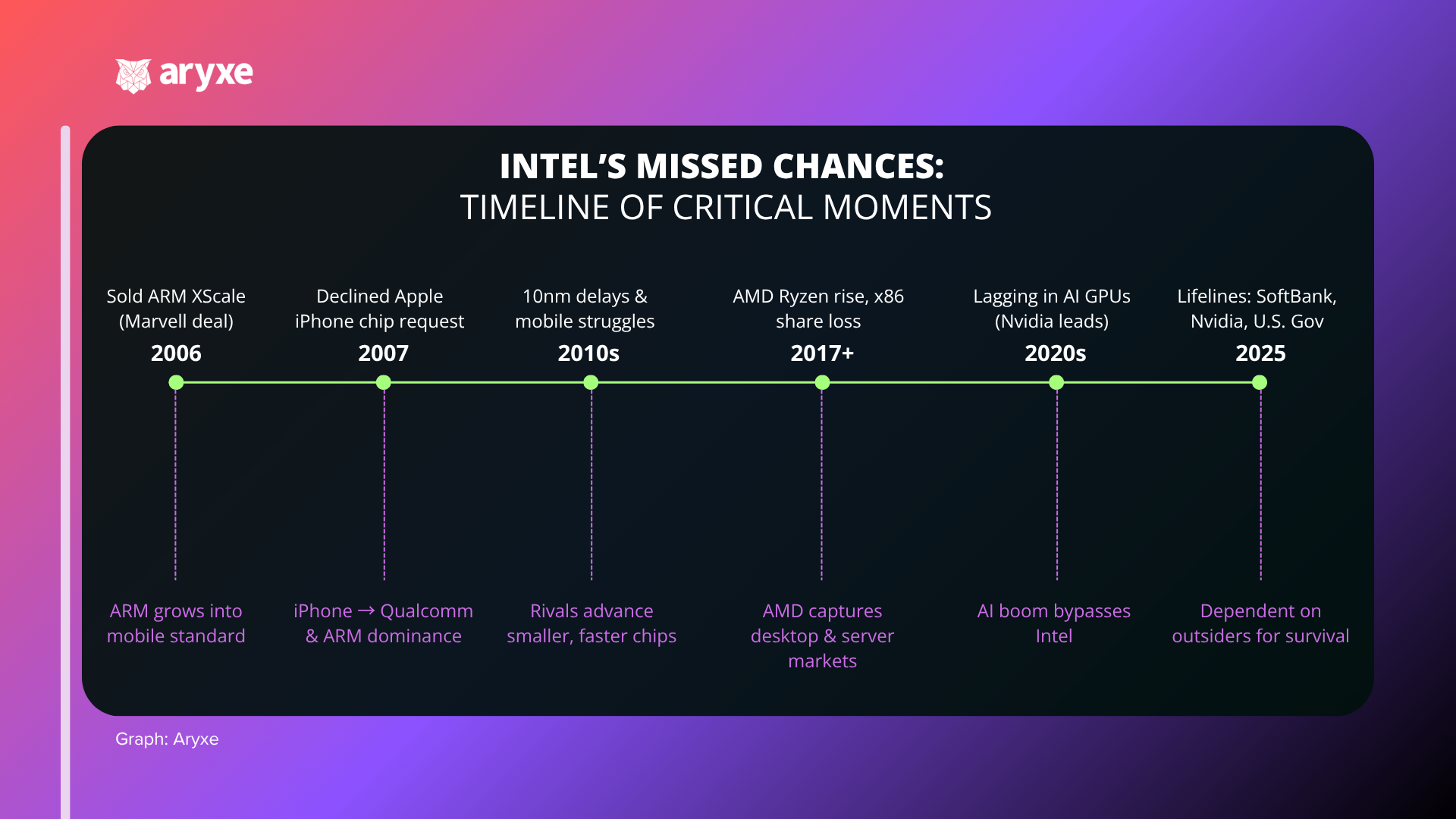

The mobile revolution is the most consequential miss. In 2007, Apple approached Intel to supply chips for the original iPhone. Intel declined — the margins weren’t attractive enough, the volumes uncertain, the power constraints not something its architecture was well-suited to. A year earlier, it had sold off XScale, its ARM-based chip design operation, rather than investing in it as a platform for the low-power, mobile-first future that was already visible on the horizon. The result: ARM-architected chips from Apple, Qualcomm, and Samsung ended up inside virtually every smartphone on the planet, and Intel was nowhere. It had passed on the chance to be inside every pocket, in favour of protecting a PC and server business that was itself about to face serious pressure.

The Apple relationship is worth pausing on. For years, Apple’s Mac line ran on Intel chips — faster and cheaper than the alternatives at the time, and a significant vote of confidence in Intel’s roadmap. Then Apple designed its own silicon. The M1 chip, launched in 2020, didn’t just match Intel’s performance in many benchmarks — it exceeded it in several, while running cooler, consuming less power, and generating less heat. The thermal management alone was a statement. Intel had not just been replaced in Apple’s laptops; it had been replaced by something demonstrably better, built by a company that had learned chip design precisely because Intel’s roadmap had stopped being reliable.

Meanwhile, two rivals had spent years sharpening their position. AMD, once permanently assumed to be in Intel’s shadow, launched its Ryzen CPU line in 2017 and spent the next eight years methodically taking share. By early 2025, AMD held around 32.2% of the desktop CPU market, up from roughly 23% the prior year, while Intel’s share had fallen to 67.8%. In server CPUs — Intel’s most profitable territory — AMD’s share climbed to 27.2% in Q1 2025, against Intel’s 72.8%, down from 76.4% just a year earlier. Among PC gamers tracked by the Steam Hardware Survey, Intel’s share has slid from around 77% five years ago to roughly 60% today. These are not rounding errors. They are a sustained, multi-year retreat across every segment Intel once owned.

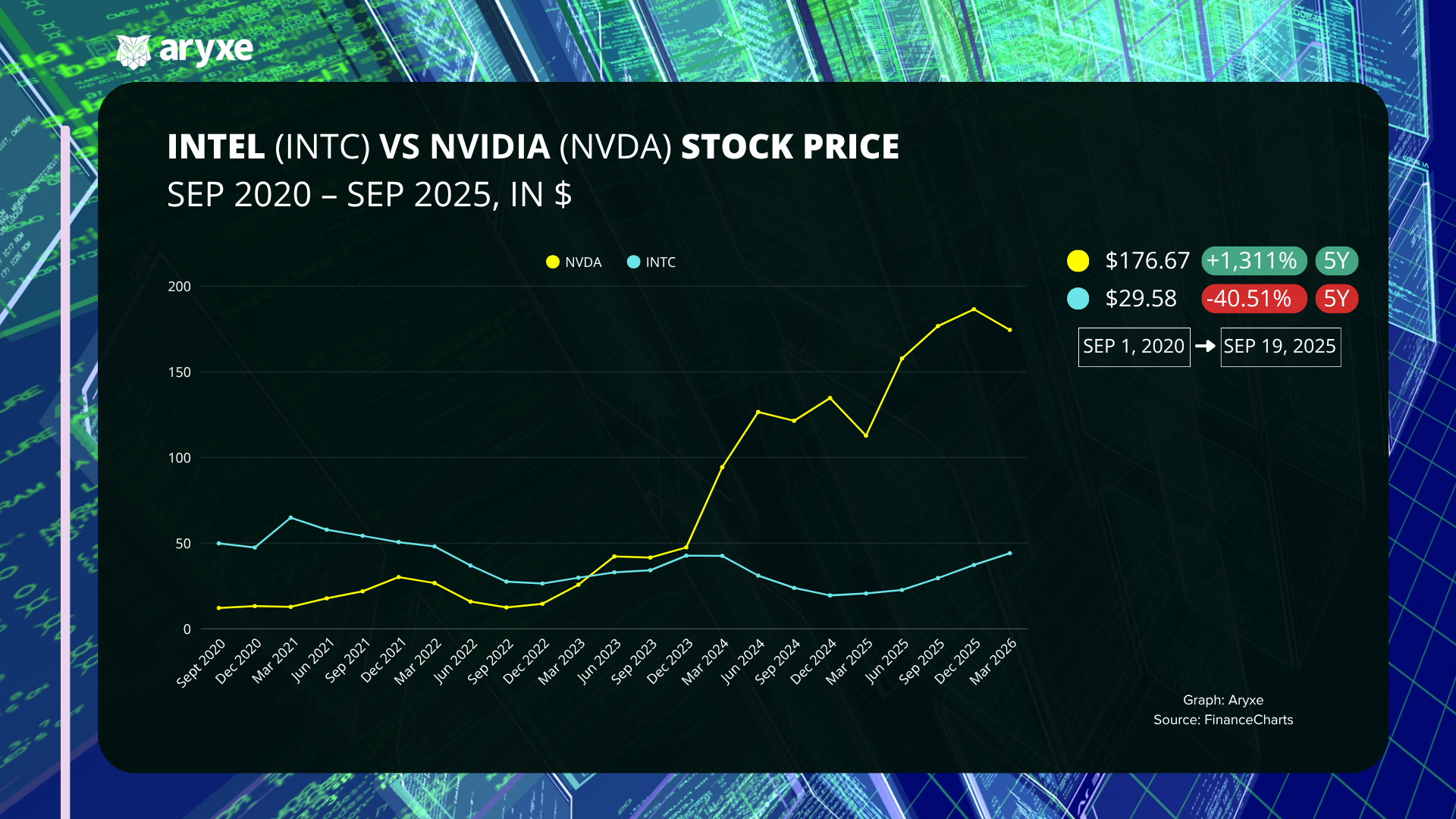

Nvidia’s ascent is the sharpest contrast of all. Intel looked at GPUs and saw a secondary market — useful for gaming, peripheral to serious computing. Nvidia looked at GPUs and saw the future of parallel processing, AI, and data centre workloads. One of them was right. By the time Intel recognised what was happening, Nvidia had built not just better chips but an entire ecosystem — CUDA, the developer tools, the relationships with every major cloud provider and AI lab — that made switching away genuinely painful for anyone who had built on it. Intel is now, somewhat surreally, a shareholder in the company that outmanoeuvred it.

Why Organisms Collapse Under Their Own Weight

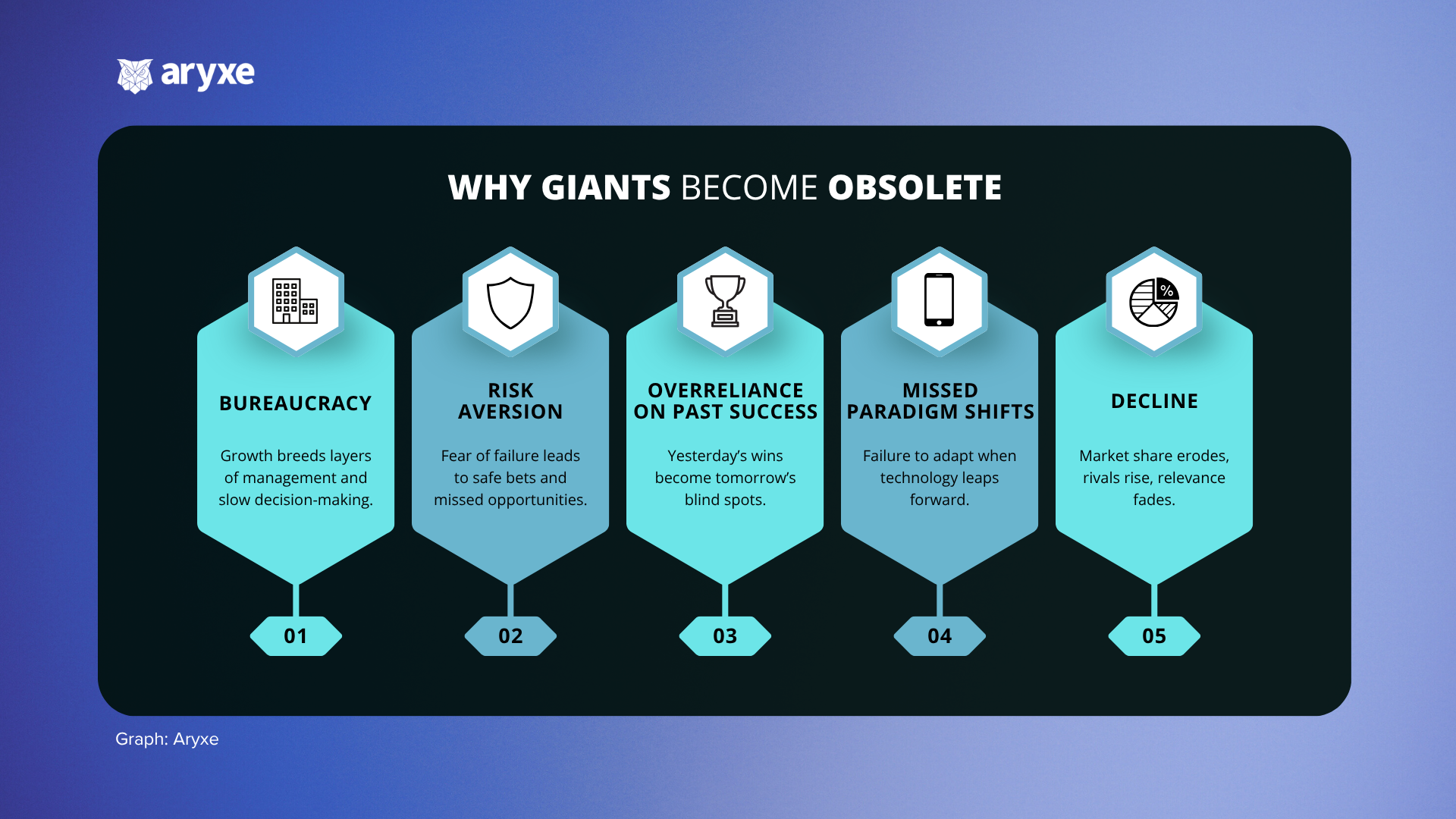

There are sophisticated frameworks and countless case studies for explaining why large companies fail at innovation — the Innovator’s Dilemma, the theory of disruptive technology, the literature on incumbent inertia. They are all essentially correct. They are also, at some level, just elaborate ways of describing something simpler.

Once an organism — plant, animal, company, country — grows beyond a certain size, it begins to collapse under its own weight. The bone structure can no longer support the mass. Decisions that once took days take quarters. The people who thrive in large organisations are increasingly not the ones who build things but the ones who navigate complexity — who know how to survive in vast organigrams, who have mastered the internal politics of a company that has more managers than engineers. The result is a progressively foggier view of the future, followed by decisions made too slowly, or not at all.

Intel built fabs — enormous, enormously expensive semiconductor fabrication plants — that were once its greatest competitive advantage and became part of its anchoring weight. TSMC, the Taiwanese manufacturer that now produces chips for Apple, Nvidia, AMD, and most of the rest of the industry, had no legacy architecture to protect, no installed base to cannibalise, and no reason to hesitate at each new process node. Intel had all three. Its manufacturing decisions were constrained by the need to protect what it already had.

This is not unique to Intel. It is the predictable outcome of scale meeting speed. The tragedy is not that Intel made irrational decisions. It is that it made entirely rational ones — and the world moved anyway.

Can Intel Come Back?

By late 2025, Intel looks less like the master of its own destiny and more like a patient surrounded by lifelines. Nvidia’s $5 billion share purchase is the most startling — the rival that took the crown now extending a hand, not out of charity but out of recognition that Intel’s manufacturing scale and x86 installed base still represent something worth preserving. SoftBank’s $2 billion adds another layer. The U.S. government’s stake looms in the background, a reminder that semiconductor manufacturing has become a matter of national security and that Washington has decided, for now, that Intel cannot be allowed to fail entirely.

These interventions give Intel oxygen. They offer time to pivot toward accelerators, to experiment with custom architectures, to rediscover the spirit that once made “Intel Inside” a seal of progress. But they also underscore the paradox: a company that once dictated the pace of innovation now survives on the faith — and funding — of outsiders.

Rescue alone is not revival. For Intel to matter again, it must transform, not just tread water. The next chapter will not be written by subsidies or alliances, but by whether Intel can rediscover what it means to move fast in a world that stopped waiting for it.

Nature, it turns out, solved the problem of organisational obsolescence long before Silicon Valley tried to. Beehives handle it with an elegance and pragmatism that no board of directors has ever matched. When a hive senses that its queen is failing — too old, too slow, no longer fit for purpose — workers build special cells called supersedure cells on the face of the honeycomb. Multiple queens are raised simultaneously as replacements. The first to hatch moves immediately through the comb and kills her rivals while they are still in their cells.

No sentiment. No severance package. No restructuring plan. Just the clean, unsentimental logic of an organism that has decided its future matters more than its past.

Intel’s lifelines — Nvidia’s billions, SoftBank’s bet, Washington’s quiet stake — may be exactly that: supersedure cells, built around the old queen by parties who have already begun to plan for what comes next. The question Intel has not yet answered is whether it intends to be the hive that survives, or the queen that gets replaced.

Sources

https://nvidianews.nvidia.com/news/nvidia-and-intel-to-develop-ai-infrastructure-and-personal-computing-products

https://www.intc.com/news-events/press-releases/detail/1746/softbank-group-and-intel-corporation-sign-2b-investment?

https://www.barrons.com/articles/intel-stock-us-trump-stake-901d516f?

https://www.techtarget.com/whatis/feature/Intels-rise-and-fall-A-timeline-of-what-went-wrong?utm_source=chatgpt.com

https://www.youtube.com/watch?v=8BaSBjxNg-M